Here are the top market developments on our radar.

INSIGHTS

Before a bounce during the last week of May, US equity prices had declined over 18% from the start of the year.

This chart shows the price performance of SPY (the SPDR S&P 500 Index ETF in blue).

While nine of the eleven equity sectors have negative returns year-to-date, most of the damage has occurred in the consumer discretionary, communication services, and information technology sectors, which have returned -24.3%, -22.3%, and -19.1% respectively. Combined these sectors constituted 51.9% of the S&P 500 Index at the beginning of the year.

This chart shows the price performance of SPY (the SPDR S&P 500 Index ETF in blue), XLK (the Technology Select Sector SPDR Fund in yellow), XLC (the Communications Services Select Sector SPDR Fund in orange) and XLY (the Consumer Discretionary Select Sector SPDR Fund in purple).

With 97% of companies having reported earnings, S&P 500 revenues increased 13.6% year-over-year. Nine sectors saw revenue growth above 7.5%, an outstanding but likely unsustainable result.

Unfortunately, expenses increased faster than revenues for many companies, so S&P 500 earnings only increased 9.2%, a 440 basis points haircut to revenue growth. In other words, profit margins declined, a result investors are worried will become a trend.

Year-over-year, net profit margins decreased for 50% of the S&P 500 companies. The financial and consumer discretionary sectors experienced the largest declines in profit margins.

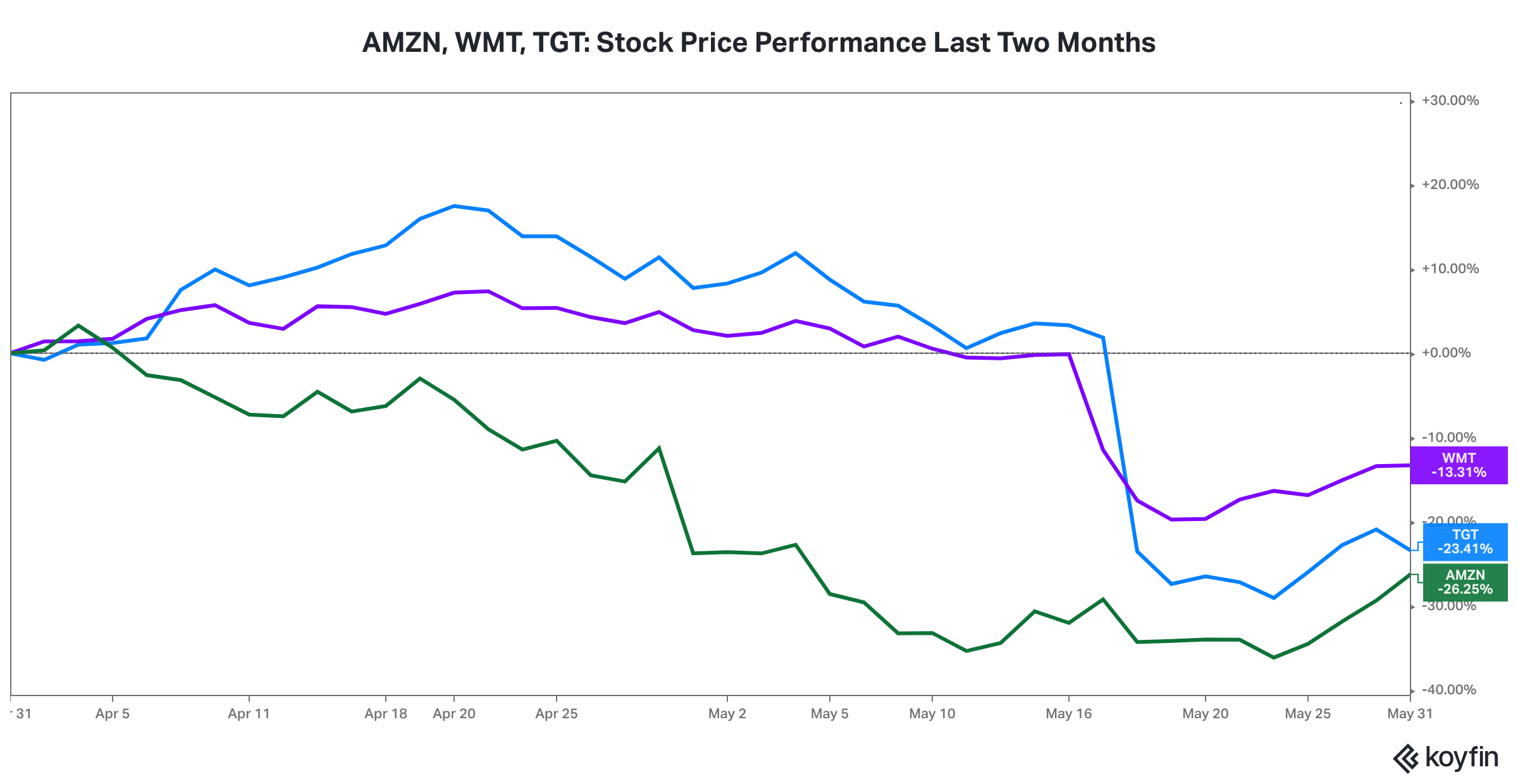

Three of the best managed consumer companies, namely Amazon, Walmart, and Target, acknowledged inventory issues, in addition to rising costs. The excess inventory will have to be marked down in price. The composition of consumer spending has shifted rapidly, particularly away from big ticket goods to services, like travel and entertainment. In addition, the rising prices of certain non-discretionary items, especially gasoline and foods, and rising home mortgage rates have put the squeeze to consumer budgets.

This chart shows the price performance of AMZN (Amazon.com, Inc. in green), WMT (Walmart Inc in purple), and TGT (Target Corporation in blue).

The ten-year Treasury yield spiked 23 basis points in the first week of May to 3.12%, representing an 160 basis point increase from the beginning of the year. That pace of increase was unprecedented, was not sustainable, and began to raise fears of monetary tightening induced recession. By month end, the ten-year Treasury yield had settled at 2.85%, just below where it ended April.

Source: treasury.gov

Credit spreads acted similarly to US equities and interest rates, moving rapidly in one direction at the beginning of the month before reversing direction. High yield spreads spiked 100 basis points from the beginning of the month through May 24, before giving back 70 basis points of the rise during the last week of the month.

The combination of rapidly rising interest rates and rising credit spreads has translated to one of the worst historical periods for bond market returns. Even US Treasuries, which outperform during recessions and crises, have generated negative returns. The worst performing segment has been long-maturity Treasuries, often considered the flight to quality asset. Depending on the benchmark, long-maturity Treasuries have generated returns in the neighborhood of negative 20% year-to-date.

A rebound in long maturity Treasury yields was not surprising given the easing of pandemic related economic restrictions, the spike in inflation, and the Federal Reserve’s stated monetary tightening plan, i.e., Fed Funds rate increases and the ending of the asset purchase program. As long as inflation moderates, we suspect most of the increase in long maturity Treasury yields is in the rear view mirror.

This chart shows the performance of AGG (iShares Core U.S. Aggregate Bond ETF in purple), JNK (SPDR Bloomberg Barclays High Yield ETF in orange), and TLT (iShares 20+ Year Treasury Bond ETF in blue).

The price of crude oil continued its march higher in May.

This chart shows the price of WTI crude oil futures.

The price of US natural gas has doubled since the beginning of the year.

This chart shows the price of US natural gas futures in mmbtu (1 Million British Thermal Units) on the New York Mercantile Exchange.

Higher energy prices (a) feed into food prices, especially via higher fertilizer costs, (b) increase expenses for most businesses, (c) reduce non-discretionary spending for most consumers, (d) raise the cost of global trade, (e) make long term planning more difficult for businesses, thus reducing management’s proclivity for longer-term, productivity investments in R&D, plant, property, and equipment, and (f) arguably raise the cost of capital via higher risk premiums, thus reducing valuations.

Given some time, the US economy and most well-capitalized companies, especially those with valuable intangible assets, can adapt to shocks, including tightening monetary policy. There may be no such thing as successfully adapting to an energy crisis.

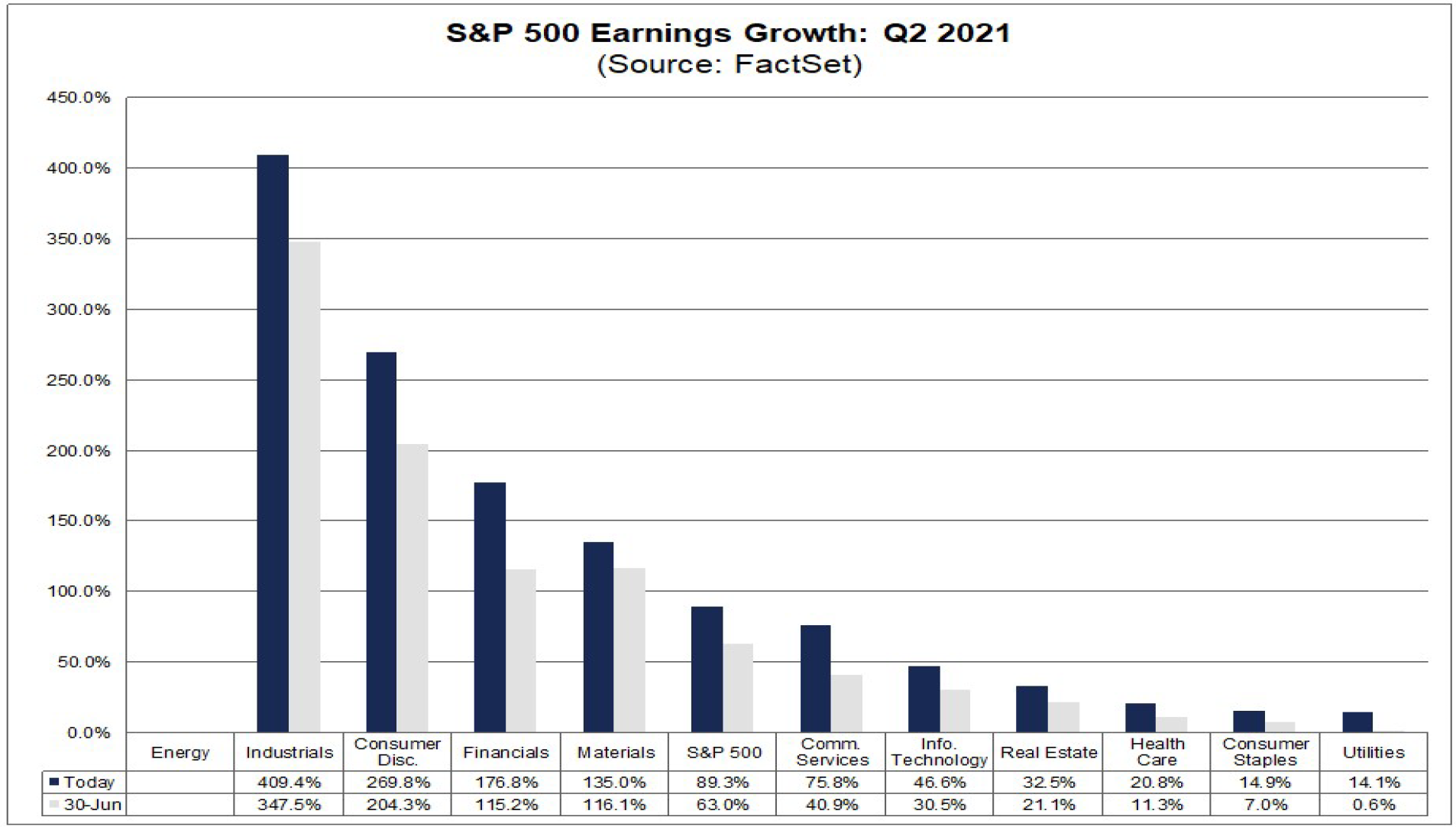

Lucky Seven is a game on the well-known show “The Price is Right”. More than luck was in play as the S&P 500 Index rose for a seventh straight month in August. Strong corporate earnings, accompanied by a favorable backdrop of accommodative monetary policy and a massive increase in fiscal expenditures, have driven a 20.4% rise in the index year-to-date. According to FactSet, S&P 500 earnings were up 89% year-over-year in the second quarter of 2021 (with 91% of companies having reported).

The US equity market is now up over 100% since the March 23, 2020 low. Some investors are starting to wonder whether the price is right, or too high, for US equities.

Second quarter earnings growth was even stronger in Europe than in the US. According to FactSet, with more than 85% of companies in the STOXX Europe 600 Index having reported, earnings are up 248% year-over-year.

Admittedly, Europe benefited more from operating leverage as the revenue differential (30% growth in Europe vs. 25% growth in the US) was much smaller than the earnings differential (248% growth in Europe vs. 89% growth in the US).

We have been warming up to non-US equities. The pricing appears to be better than US equities. For instance, while European equities usually trade a lower P/E multiple than US equities, they are currently trading around six multiple points lower than the US, European earnings growth has accelerated past US earnings growth, and European equities have underperformed US equities by over 25% since the March 23, 2020 pandemic low. A performance catch up is starting to seem more plausible.

Source: Yardeni Research

This chart shows forward Price / Earnings ratios for different regions, using MSCI index data.

US value stocks outperformed US growth stocks for the first five months of the year as an economic activity boom with accelerating inflation was the dominant narrative. However, over the three months ending in August, growth stocks have staged a big comeback. The narrative has started to shift from a fear of inflation to a concern about the sustainable level of revenue growth.

The graph shows the total return for the iShares Russell 1000 Growth ETF (IWF) in orange and the iShares Russell 1000 Value ETF (IWD) in purple for the three months ending in August 2021.

Of the four questions we have raised, we have the most conviction in answering the last question. Yes, the compensation for credit risk is too low. It might be Bonkers (“The Price Is Right” show has a game by that name). Certainly, the monetary and fiscal stimulus over the last year and a half has boosted economic activity and spared many businesses from more negative outcomes. The US commercial banking system is also in excellent health. The sharp decline in credit spreads from the pandemic highs reflects the uptick in prospects for many non-financial businesses and the strong capital position of the banking system.

Source: St. Louis Federal Reserve Economic Data

This chart shows ICE BoFA High Yield Bond Index credit spreads from December 1996 - August 2021.

However, high yield bond spreads are near the lows of the last 25 years, at a time when interest rates are also near secular lows, debt levels are at a record high for the non-financial business sector, and trend rate of growth of economic activity is lower because productivity has not been able to offset a declining labor participation ratio. While we do not see an immediate cause for the concern, a shock that precipitates a rapid rise in debt costs may not be as manageable for the overall economy as it was in the past. Fragility has increased.