1. The global equity market weakness continued for another month in October, likely triggered by the jump in long maturity U.S. Treasury yields.

This chart shows the performance of SPY (SPDR S&P 500 Index ETF in purple), EFA (iShares MSCI EAFE ETF in blue), EEM (iShares MSCI Emerging Markets ETF in orange) and IWM (iShares Russell 2000 ETF in grey), and TLT (iShares 20+ Year Treasury Bond ETF in dashed red).

2. The U.S. Treasury yield curve continued its bear steepening behavior. Long maturity U.S. Treasury yields jumped, while short maturity U.S. Treasury yields barely moved.

Since the end of August, the ten-year U.S. Treasury note yield has risen 76 basis points, while the two-year U.S. Treasury note yield has risen a paltry 17 basis points, representing a steepening of 59 basis points.

Source: treasury.gov, Two Centuries Investments

A bear steepening is commonly defined as a double-digit basis point increase in the difference between the 10-year Treasury and 2-year Treasury yield. A bear steepening is a rare occurrence, especially when the yield curve is inverted like it is currently.

The table below from Janus Henderson illustrates the historical rarity.

· The orange highlighted rows map to bear steepening off inverted yield curves.

· The blue highlighted rows map to bear steepening off relatively flat curves.

· The green highlighted rows map to bear steepening off very steep curves.

What message could the bond market be communicating?

Are the “bond vigilantes” back, demanding higher yields to protest the Federal Reserve’s policies, as they supposedly did during the early 1980s according to economist Ed Yardeni, who coined the “bond vigilante” phrase?

Are the “bond vigilantes” back like they supposedly were during the 1994 Great Bond Massacre, protesting concerns about federal government spending levels? During the 1994 crisis, Clinton Administration political adviser James Carville referenced the “bond vigilantes” when he said, "I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody."

We argue the current situation is a straightforward supply and demand issue. The bond market sees ongoing large auctions of Treasury notes and bonds on the horizon, as federal government spending remains at elevated relative to a few years ago, federal tax revenues have been in decline since the end of 2022, and the U.S. Treasury Department shifts away from its reliance on Treasury bill issuance. There will be a jump in the supply of longer maturity notes and bonds.

What about buyers, i.e., demand, for the increased supply? Most importantly, the Federal Reserve ended its Quantitative Easing program and is reducing the size of its balance sheet. It was a big buyer of Treasuries, and a price insensitive one at that. China and Japan have curtailed their purchases of Treasuries, whether for geo-political or domestic reasons. U.S. banks already have too much interest rate duration as the regional bank crisis highlighted in March 2023. Defined benefit pension funds and traditional life insurers, once large natural buyers of long maturity Treasuries, are in decline.

Price sensitive buyers realized they can garner more income on Treasury bills and short-term Treasury notes than longer maturity Treasury notes and bonds. A 5+% rate also feels good after years of near zero short term rates. Yes, cash equivalents pose reinvestment risk, but the other side of the coin is assuming considerable duration risk when inflation is not yet back to its low and stable pre-pandemic levels.

In summary, the bond market is likely communicating a supply digestion concern, The problem is higher long maturity interest rates at this stage of the economic cycle create tighter financial conditions, especially for the housing market which is largely financed by fifteen-year and thirty-year mortgage loans. Home construction and renovation have been large contributors to economic growth. In summary, the incremental tightening of financial conditions reduces the probability of a soft landing for the economy.

3. As we keep repeating, what lies ahead for financial markets will likely be driven by the path and composition of inflation.

The concern about inflation has likely contributed to the bear steepening of the yield curve and the tighter financial conditions. Inflation has historically impacted equity valuation multiples. High inflation has led to lower multiples and thus lower investment returns. The composition of inflation will also impact earnings. The last few decades have been a period of low growth in labor costs and low energy costs, both major drivers of rising corporate profit margins.

The headline inflation rate has dropped to about 1% above pre-pandemic levels but has risen over the last three months.

The concern is the “core” inflation rate (excludes food and energy) has proven stickier and remains 2% above pre-pandemic levels. If not for the ongoing bear steepening of the yield curve, the sticky core inflation rate might compel the Federal Reserve to keep raising short term interest rates in an attempt to dampen economic demand and push inflation back towards its 2% target.

4. Despite the Federal Reserve raising the federal funds rate by 5% over the last eighteen months, real economic growth has not collapsed, though it remains muted.

Real gross domestic product (GDP) and real gross domestic income (GDI) have diverged over the last few quarters. GDP data shows the economy humming along, while GDI data points to an economic slowdown.

5. The challenge the Federal Reserve faces is how to balance its dual mandate of maximum employment and stable (2% target) inflation.

In the current economic environment. the Federal Reserve cannot achieve its inflation target without risking a significant rise in unemployment and a recession. Because of structural supply shortages, most notably in the labor market, tighter monetary policy is less effective in reducing inflationary pressures. Tighter monetary policy operates by increasing the cost of debt capital and thus, with a lag, puts downward pressure on the demand for goods and services. The dilemma is the Federal Reserve may have to risk crushing real GDP growth (the volume of goods and services being transacted) in order to crush inflationary pressures (price of goods and services being transacted).

While the Federal Reserve Bank of Atlanta data shows wage growth across all industries continues to slow, there are many industries facing supply shortages. Recently, United Airlines and American Airlines pilots were able to negotiate 40% wage increases over the next four years. UPS union employees negotiated wage increases near 20% over five years and the UAW (United Auto Workers) negotiated 25% general pay increases plus cost-of-living adjustments over the next four years for the Big 3 auto workers.

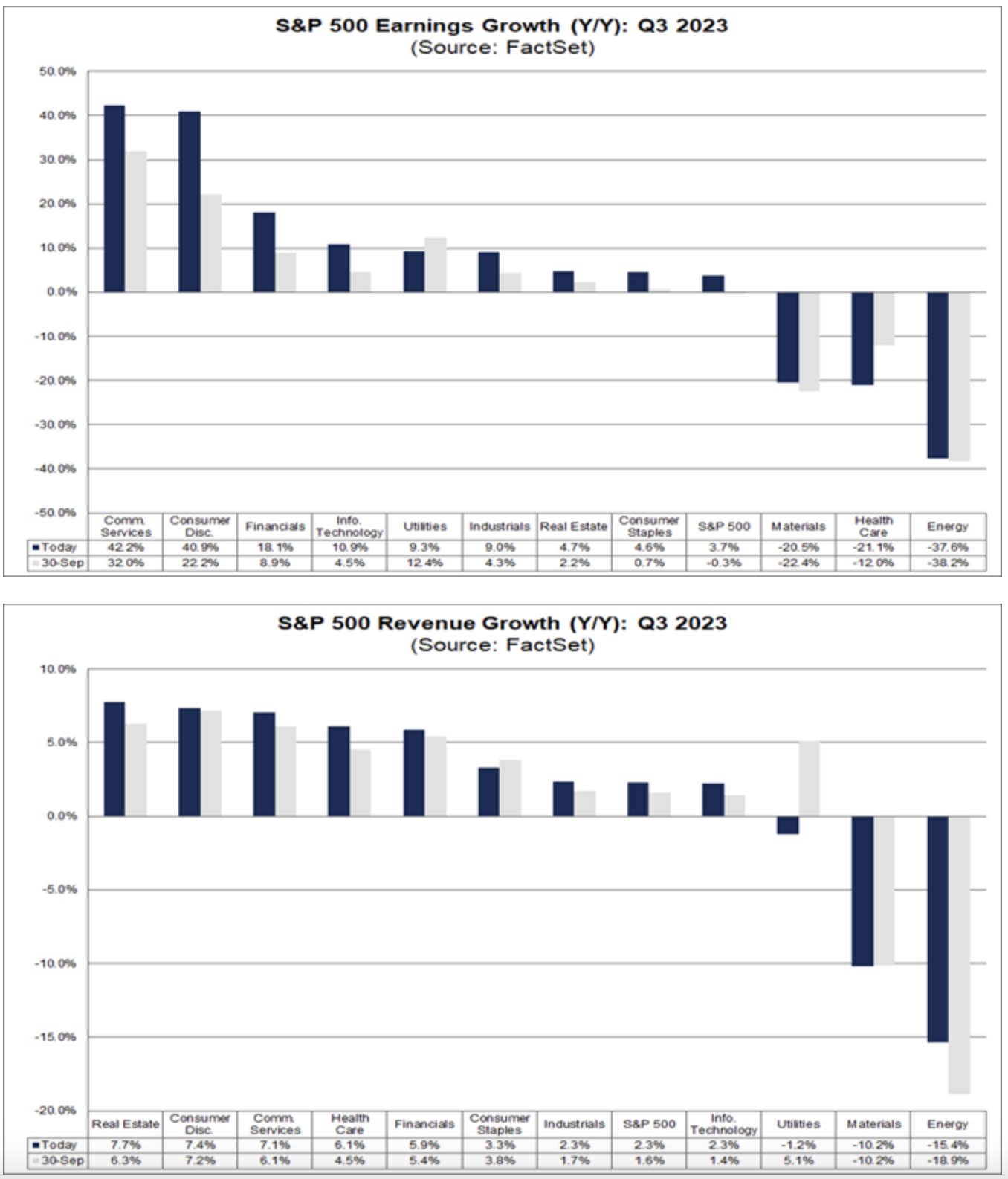

6. The S&P 500 Index may achieve year-over-year earnings growth, an outcome last seen in the third quarter of 2022.

With 81% of the companies in the index having provide quarterly earnings reports, the earnings growth rate is tracking at 3.7% year-over-year, while the revenue growth rate is 2.3%.

7. Credit markets remain sanguine despite the Federal Reserve’s actions to tighten monetary policy and the recent bear steepening.

High yield bond spreads remain near long term averages and below recent peaks.